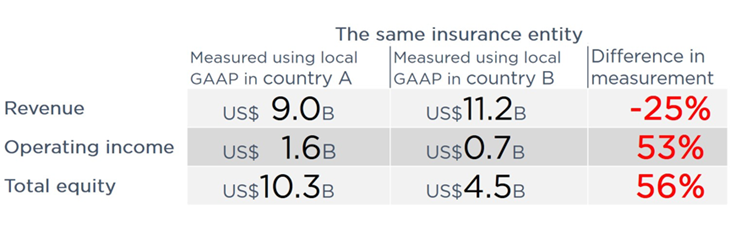

IFRS 17 will make insurers in different countries comparable for the first time

IASB has been working IFRS 17 (previously IFRS 4 Phase II) since 2005. It will become effective in 2022. The principal aim of the standard is to eliminate the kinds of differences seen in the above illustration. In a recent meeting, IASB made a concession to insurers that they would only be required to provide one set of ‘pre IFRS 17’ accounts for 2023. So investors will be left with a total of 2 years’ worth of comparative information to inform the changing nature of insurers’ performance.

This standard will fundamentally change how insurers measure themselves and will require a substantial shift in their business management and back-office operating models. The balance sheets of insurers will radically change and so therefore will investor perception and market valuation of insurers.